HOW DID THE SUBPRIME LOAN MESS GET TO THIS POINT?

Sub prime mortgage loans have created a financial mess that this country has not seen since the early 1980's when mortgage rates reached 20% on conventional mortgages and subsequently put many banks and savings  and loans out of business because they had too many fixed rate loans guaranteed at very low interest rates. Now sub prime loans have put 30 of the top 100 mortgage lenders in the nation out of business and have caused many large financial companies to take billions of dollars in losses, including Morgan Stanley, Citibank, Merrill Lynch and Countrywide Mortgage, the nation's largest mortgage company.

and loans out of business because they had too many fixed rate loans guaranteed at very low interest rates. Now sub prime loans have put 30 of the top 100 mortgage lenders in the nation out of business and have caused many large financial companies to take billions of dollars in losses, including Morgan Stanley, Citibank, Merrill Lynch and Countrywide Mortgage, the nation's largest mortgage company.

and loans out of business because they had too many fixed rate loans guaranteed at very low interest rates. Now sub prime loans have put 30 of the top 100 mortgage lenders in the nation out of business and have caused many large financial companies to take billions of dollars in losses, including Morgan Stanley, Citibank, Merrill Lynch and Countrywide Mortgage, the nation's largest mortgage company. From late 2001 until 2005, mortgage lenders had a huge refinancing boom as rates declined. Then refinancing came to a halt abruptly. Many lenders, especially mortgage companies were wondering how they would stay in business. Unlike banks, mortgage companies do not have their own money to lend; they borrow money on a short term basis and resell the loan shortly after they originate the loan. Their profit is derived from origination fees, discount points and closing costs, but this income stream suddenly decreased when the refinance boom ceased, so they became more creative. They lowered the down payment requirement from 10% to 0%. They offered teaser rates to borrowers a full 3% below the market rates and they loosened the qualifying criterion to make it easier for buyers to qualify. The long standing qualifying income and debt ratios of 28% income and 36% debt ratios were relaxed. They also entered into providing sub prime loans to borrowers with poor credit histories; these people previously were denied home mortgage loans. The teaser rates offered are similar to the zero-down, zero-interest rates offered by auto dealer and furniture stores. They are designed to get buyers to purchase homes and get mortgages. The problem is the teaser rates only last one year to three years then they automatically reset to market rates. The difference in payments can be shocking to the homeowner. For example, monthly payments on a $200,000, 30-year mortgage at 3% would be $844 for principal and interest. At 5%, the payment increases to $1,074. If it goes up to a typical sub prime rate of 9%, the payments are $1,610, that's up $766 a month from the teaser rate, or $9,192 per year.

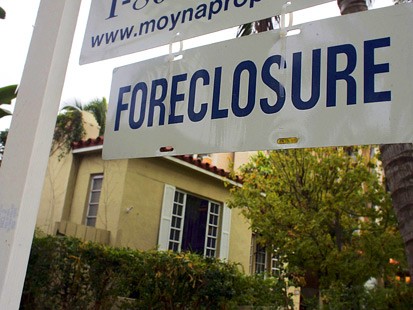

The large jump in mortgage payments has increased the home foreclosures dramatically in the past two years. And making sub prime loans to people with poor credit histories and low credit scores is another culprit. In fact, when the sub prime loan industry began offering loans to buyers with below average or poor credit histories, they required larger than normal down payments to protect themselves against foreclosure losses. But they quickly realized that most people with below average or poor credit histories cannot put 30% down on a home, so the aggressive lenders lowered the down payments to 20%, 10% and eventually 0%. This lowering of underwriting standards is one of the prime causes in mortgage firms going out of business. They made loans to people who were huge credit risks and they did not get adequate down payments to cover the potential foreclosure losses.

When a sub prime borrower is suddenly faced with an increase of $700 or more a month, as in the above example, he simply cannot pay the higher monthly payment and stops paying. The lender is forced to foreclose and the lender is often required to buy back the sub prime loan, if it is foreclosed on in the first two years. Since mortgage companies are unlike banks and do not have large sums of money available to buy back the foreclosed home, the mortgage companies are forced out of business. Countrywide Mortgage, the largest mortgage lender in the U.S., was thought to be invulnerable to going out of business, but they made too many sub prime loans, which forced them to borrow $20 billion dollars in the summer of 2007 to stay in business. In January 2008, with losses still coming, they were about to take bankruptcy, when Bank of America agreed to purchase them for about 25% of their value a year earlier.

Mortgage lenders are not the only culprits in the sub prime and foreclosure situation we have today. Property values in California, Arizona, Florida and Nevada doubled in 5 years, making payments out of reach for some homeowners, but they wanted homes so bad they purchased properties they could not really afford, hoping they would continue to appreciate in value. In 2006, prices started to come down in these over-inflated areas and caused many homeowners to have mortgage loans greater than the value of the home. This makes the property almost impossible to sell, which in turn has caused many foreclosures. Many individuals wanted to own their own home so much, that they purchased properties they had no business purchasing. Plus many Americans live way above their means with fancy cars and all the trimmings of wealth. They were able to afford those luxuries while their homes were appreciating in double-digits each year, but that simply is not happening today. Homeowners who have no equity in the property and can't afford the payments simply walk away from the homes. So there are many reasons and culprits for the current mortgage mess.